NASA’s Continuing Lack of Accounting Controls

Jed Margolin

1. In 2002 GAO assessed NASA’s financial

management system as inadequate, but NASA was working on a new financial

management system (its third attempt) and expected it to be fully functional in

2008. It hasn’t happened even though, for a time, NASA’s administrator was an

accountant (Sean O’Keefe - December 2001 to February 2005).

Reference 1 - GAO Testimony Before the Committee on Science,

Subcommittee on Space and Aeronautics, House of

Representatives, NASA MANAGEMENT CHALLENGES, Human Capital and Other Critical

Areas Need to be Addressed, Statement of David M. Walker, Comptroller General

of the United States,

July 18, 2002.

http://www.dtic.mil/cgi-bin/GetTRDoc?AD=ADA404576&Location=U2&doc=GetTRDoc.pdf

{Click here for Local Copy}

From page 23 - page 24 (I have underlined what I think is important):

The inadequacy of NASA’s financial management

system has further impact. Without a more effective financial management

system, NASA will likely continue to have difficulty providing relevant,

reliable, timely financial data -including cost information- that can be used

on a real-time basis by program managers to monitor costs, schedule, and

performance. In March 2002, we testified9 that NASA was unable

to provide us with detailed support for amounts obligated against cost limits

established by the fiscal year 2000 NASA Authorization Act. This was due, in

large part, to NASA’s lack of a modern, integrated financial management system.

To its credit, NASA is working toward implementing

an integrated financial management system that it expects to be fully

operational in fiscal year 2008 at an estimated cost of $691 million. This

is NASA’s third attempt toward implementing a new integrated financial

management system. The first two efforts were abandoned after 12 years and

after spending a reported $180 million. NASA’s current approach focuses on

learning from other organizations’ successes in implementing similar projects,

as opposed to revisiting its own failures. NASA has also abandoned the single

product approach that the two prior attempts had as their basic architecture.

Instead, the project will be broken down into implementable modules on the

basis of the availability of proven software products.

2. In January 2004, the

independent auditor -PricewaterhouseCoopers- conducting NASA’s audit pursuant

to the Chief Financial Officers Act and under the direction of the Office of

Inspector General, determined that it could not render an opinion on NASA’s

financial statements for FY 2003. The disclaimer resulted from NASA’s inability

to provide the auditor with sufficient evidence to support the financial

statements and complete the audit within time frames the Office of

Management and Budget established. The disclaimer on the FY 2003 financial

statements followed an unqualified1 FY 2002 audit opinion and a

disclaimed audit opinion in FY 2001.

Reference 2 - Testimony of NASA Inspector General, May 19, 2004

http://oig.nasa.gov/congressional/Testimony051904.pdf {Click here for Local Copy}

Before the

Government Reform Subcommittee on Government Efficiency and Financial Management

U.S. House of Representatives, May 19, 2004, NASA Financial Management

Statement of The Honorable Robert W. Cobb, Inspector General National

Aeronautics and Space Administration.

From page 2:

OVERALL

SUMMARY

In

January 2004, the independent auditor—PricewaterhouseCoopers—conducting

NASA’s audit pursuant to the Chief Financial Officers Act and under the

direction of the Office of Inspector General, determined that it could not

render an opinion on NASA’s financial statements for FY 2003. The disclaimer

resulted from NASA’s inability to provide the auditor with sufficient

evidence to support the financial statements and complete the audit within

time frames the Office of Management and Budget established.

The

disclaimer on the FY 2003 financial statements followed an unqualified1 FY 2002 audit opinion and a disclaimed audit

opinion in FY 2001. The FY 2002 unqualified opinion was the consequence of

a so-called “heroic” effort of the independent auditor PricewaterhouseCoopers.

A heroic audit effort occurs where assurance on the financial statements is

established through substantially expanded transaction testing rather than the

auditor placing reliance on systems of internal control. Such a heroic effort

was not possible in FY 2003 because of dependency on a new automated financial

management system.

The reports that the independent auditor submitted

identified instances of non-compliance with generally accepted accounting

practices, material weaknesses in internal controls, and non-compliance with

the Federal Financial Management Improvement Act. Many of the weaknesses the

audit disclosed resulted from a lack of effective internal control procedures

and problems with NASA’s conversion during FY 2003 from 10 separate systems to

a new single integrated financial management program (IFMP).

Mr. Cobb’s testimony was in 2004.

An article

in the Orlando Sentinel on November 20, 2006 by Michael Cabbage,

Sentinel Space Editor, sheds some light on NASA’s accounting problems. Investigators from the Department of Housing and Urban

Development were called in to conduct an inquiry into complaints made by career

employees in Cobb’s own office. (I wonder why HUD conducted the investigation

and not DOJ.)

From the Orlando

Sentinel article:

According to the probe, the number

of audit reports issued by Cobb's office plummeted from 62 in 2000 to seven

during the first half of the 2006 fiscal year. An audit safety team was

abolished. Investigations were derailed, witnesses said, including some related

to safety and national security.

Investigators found that Cobb lunched, drank, played golf and traveled with

former NASA Administrator Sean O'Keefe, another White House appointee. E-mails

from Cobb showed he frequently consulted with top NASA officials on

investigations, raising questions about his independence.

.

.

.

Nicknamed "Moose," Cobb

came to NASA in April 2002 after 15 months as an ethics lawyer in the Bush

White House responsible for vetting financial-disclosure and

conflict-of-interest issues for administration nominees who required Senate

confirmation. He replaced Roberta Gross, a Clinton appointee, who had been in the job

since 1995 and had earned a reputation on Capitol Hill as a competent,

independent investigator.

The HUD report discusses Gross' departure from NASA.

Gross had contracted with the accounting firm Price Waterhouse Coopers to do

NASA's chief financial audit, investigators wrote. After the White House tapped

O'Keefe to succeed longtime NASA Administrator Dan Goldin in December 2001,

O'Keefe told Gross he was unhappy with the audit. "Gross subsequently

[was] asked to resign," the report said.

Cobb replaced Gross four months after O'Keefe's arrival and canceled the

contract with Price Waterhouse Coopers.

HUD investigators heard testimony from other witnesses that suggested O'Keefe's

and Cobb's association went beyond the traditional arm's-length relationship

between agency heads and inspectors general. E-mail traffic between Cobb,

O'Keefe and former NASA General Counsel Paul Pastorek indicated Cobb consulted

with them on audits and investigations.

.

.

.

In one case, Cobb was accused of

squelching part of an audit related to the international space station program

after conferring with Pastorek. The report notes that investigators found an

e-mail where Pastorek wanted to discuss the audit and questioned its analysis

and conclusions. Investigators wrote that auditors were told to remove all of

the findings from one section, reducing four pages of findings in the draft

report to one paragraph in the final version.

.

.

.

According to witnesses in the HUD

report, Cobb told his staff, as well as an outside group, that he had to do

some "diving saves" to keep his auditors from embarrassing NASA.

See http://www.orlandosentinel.com/news/space/orl-nasa-inspector-files7,0,3895863,full.story

{Click here for Local Copy}

Mr. Cobb protested his innocence.

Despite calls by Senator Jay Rockefeller (D-WV) and Senator Bill Nelson

(D-FL) for Cobb to resign, he refused to do so until April 2009.

http://commerce.senate.gov/public/index.cfm?p=PressRoom&ContentType_id=77eb43da-aa94-497d-a73f-5c951ff72372&Group_id=505cc3fa-a767-40f4-8ac2-4b8326b44e94&MonthDisplay=4&YearDisplay=2009

COMMERCE CHAIRMAN ROCKEFELLER’S STATEMENT ON

RESIGNATION OF NASA INSPECTOR GENERAL ROBERT COBB

Jena Longo - Democratic Deputy

Communications Director 202.224.7824

Apr 02 2009

COMMERCE CHAIRMAN ROCKEFELLER’S STATEMENT ON

RESIGNATION OF NASA INSPECTOR GENERAL ROBERT COBB

WASHINGTON, D.C. – Senator John D (Jay)

Rockefeller IV (D-WV), Chairman of the U.S. Committee on Commerce, Science and

Transportation, issued the following statement regarding the resignation of

NASA Inspector General Robert Cobb:

“Only a few short weeks ago, Senator McCaskill and

I expressed deep concerns to President Obama that the NASA Inspector General,

Robert Cobb, had been repeatedly accused of stifling investigations,

retaliating against whistleblowers and prioritizing social relationships with

top NASA officials over proper federal oversight. I respectfully asked that the President take

immediate action to put an end to IG Cobb’s conflict of interest and cronyism

and remove him from the system.

“News of Robert Cobb’s resignation is certainly

welcome and this is an important step forward.

I applaud the White House for taking a zero tolerance approach to lax

enforcement and oversight. President

Obama is setting the tone from the top and holding all employees who serve the

American people accountable for improper conduct and just plain not doing their

jobs. The time has come to close the

door on this troubling chapter for NASA and a fresh start awaits.”

***(SEE ATTACHED LETTER)***

###

If you want to know what it was like to work for Cobb see the Oral

Statement made to the Oversight Review of the Investigation of the NASA

Inspector General Mr. Robert W. Cobb by Lance G. Carrington

,

Former Assistant Inspector General for Investigations, NASA Office of

Inspector General:

http://legislative.nasa.gov/hearings/2007%20hearings/6-7-07%20carrington.pdf {Click here for Local Copy}

Here is more from the hearings: http://www.agiweb.org/gap/legis110/nasa_hearings.html#june7

The reason for including this material here is because the problems

Cobb reported in his testimony to Congress in 2004 were problems that he

himself created or was complicit in creating.

3. In 2008 NASA was unable to account for capital

assets with an acquisition cost of about $32 Billion (with a net value of about

$18.6 Billion). It was worse than that.

As part of its FY 2007 report on NASA’s financial statement,

E&Y, in its “Report on Internal Control,” dated November 13, 2007,

identified significant deficiencies that it considered to be material

weaknesses under standards established by the American Institute of Certified

Public Accountants. E&Y identified material weaknesses in NASA’s controls

for financial systems, financial analyses, oversight used to prepare the

financial statements, and

processes for assuring that PP&E and materials are presented fairly in the

financial statements. In addition, E&Y stated that NASA’s financial

management systems are not substantially compliant with the Federal Financial

Management Improvement Act (FFMIA) of 19962 noting that certain subsidiary systems, including all

property systems, are not integrated with NASA’s Systems Applications and

Products (SAP) Core Financial module. Core Financial—customized off-the-shelf

software that serves as the backbone to the IEMP—is used to record accounting

transactions including commitments, obligations, and expenditures and to

produce NASA’s annual financial statements

.

Reference 3

-

Report No. IG-08-032 - http://oig.nasa.gov/audits/reports/FY08/IG-08-032.pdf {Click here for Local Copy}

September 25, 2008

TO: Chief Financial Officer

Chief Information Officer

Deputy to Chief Information Officer

Director, Marshall Space

Flight Center

FROM: Assistant Inspector General

for Auditing

SUBJECT: Final Memorandum on NASA’s

Development of the Integrated Asset Management – Property, Plant, and Equipment

Module to Provide Identified Benefits (Report No. IG-08-032; Assignment No.

A-08-001-00)

From page 1:

The Office of Inspector General conducted an audit of NASA’s Integrated

Asset Management – Property, Plant, and Equipment (IAM/PP&E) module. A component of NASA’s Integrated Enterprise

Management Program (IEMP), the IAM/PP&E module is an automated asset-management

system that performs two main functions: equipment management (logistics) and

asset accounting (finance) and was designed to integrate logistics and

financial processes to account for and facilitate management of NASA personal

property.

From page 2:

Executive Summary

We found that NASA adequately

defined the IAM/PP&E module project requirements to ensure the six benefits

are achieved and that the achievement would be measurable. To determine

that the project requirements were adequately defined, we verified that the

requirements were crosswalked to each anticipated benefit; we verified that

project personnel had reviewed the Federal financial system requirements and

could trace the project requirements to the Federal requirements; and we reviewed

the project’s Performance Measurement Plan to verify that a performance measure

could be tied to each of the six identified benefits. We determined that the

IAM/PP&E module, as designed, and the corresponding changes in NASA’s

business processes and controls should help mitigate deficiencies reported as

material weaknesses by Ernst and Young (E&Y), the independent public

accounting firm that conducted the audit of NASA’s financial statements for the

past 4 years.

However, also from page 2:

We note, however, that the

system’s contribution to improved financial reporting may be limited by

inaccurate data. NASA did not validate approximately 6,300 records of capital

assets that have an acquisition value of $32 billion (and a net value of

approximately $18.6 billion) prior to transferring the data into IAM/PP&E.

In addition, NASA has not resolved an operating policy issue involving

identifying purchases of controlled equipment, which could bear on the

successful operations of the system. However, we did not conduct audit work to

address the impact of these issues because E&Y plans to perform tests of

the IAM/PP&E module and NASA’s corresponding manual controls as part of the

fiscal year (FY) 2008 financial statement audit. Accordingly, we made no

recommendations for management action. We issued a draft of this memorandum on

September 17, 2008, and provided NASA management an opportunity to comment on

the draft, but comments were not required and no formal comments were received.

And, from page 2 - page 3

Background

As part of its FY 2007 report on

NASA’s financial statement, E&Y, in its “Report on Internal Control,” dated

November 13, 2007, identified significant deficiencies that it considered to

be material weaknesses under standards established by the American Institute of

Certified Public Accountants. E&Y identified material weaknesses in

NASA’s controls for financial systems, financial analyses, oversight used to

prepare the financial statements,

and processes for assuring that PP&E and materials are presented fairly in

the financial statements. In addition, E&Y stated that NASA’s financial

management systems are not substantially compliant with the Federal Financial

Management Improvement Act (FFMIA) of 1996,2 noting that certain subsidiary systems, including all

property systems, are not integrated with NASA’s Systems Applications and

Products (SAP) Core Financial module. Core Financial—customized off-the-shelf

software that serves as the backbone to the IEMP—is used to record accounting

transactions including commitments, obligations, and expenditures and to

produce NASA’s annual financial statements.

Therefore,

NASA’s response to the criticism that it is not following the accounting

procedures established by the American Institute of Certified Public

Accountants was to cook the books.

4.

FY 2009 was not much better. From Acting Inspector General Thomas J.

Howard:

“Although much progress has been made in developing

policies, procedures, and controls to improve NASA’s financial processes and

systems, challenges remain. Specifically, during FY 2009, NASA management and

Ernst & Young LLP (E&Y) continued to identify deficiencies in the

Agency’s system of internal control, which impair NASA’s ability to timely

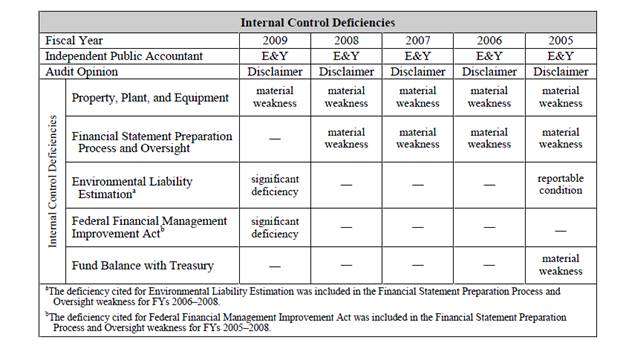

report accurate financial information. The most severe deficiency involves

NASA’s internal control over legacy property, plant, and equipment (PP&E).

As shown in the following table, this deficiency has been reported as a

material weakness for several years.”

Reference 4 - NASA 2009 Management

Challenges http://oig.nasa.gov/NASA2009ManagementChallenges.pdf {Click here for Local Copy}

Cover

Letter:

November 13, 2009

TO: Administrator

FROM: Acting Inspector General

SUBJECT: NASA’s Most Serious Management and Performance

Challenges

As required by the Reports Consolidation Act of 2000, this

memorandum provides our views of the most serious management and performance

challenges facing NASA and is to be included in the Agency’s Performance and

Accountability Report for fiscal year 2009.

In determining whether to report an issue as a challenge,

we consider the significance of the issue in relation to the Agency’s mission;

its susceptibility to fraud, waste, and abuse; whether the underlying problems

are systemic; and the Agency’s progress in addressing the issue. We provided a

draft copy of our views to Agency officials and considered all comments

received.

Through various Agency initiatives and by implementing

recommendations made by the Office of Inspector General (OIG) and other

evaluative bodies, such as the Government Accountability Office, NASA is

working to improve Agency programs and operations. However, challenges remain

in the following areas:

• Transitioning from the Space Shuttle to the Next

Generation of Space Vehicles

• Managing Risk to People, Equipment, and Mission

• Financial Management

• Acquisition and Contracting Processes

• Information Technology Security

During FY 2010, the OIG will continue to conduct work that

focuses on NASA’s efforts to meet these challenges as part of our overall

mission to promote the economy and efficiency of the Agency and to root out

fraud, waste, abuse, and mismanagement.

We hope that you find our views helpful. Please contact me

if you have questions.

signed

Thomas J. Howard

From

page 5 - page 6:

Financial Management

Over the past year, NASA continued to make progress in

improving its internal control over financial reporting by executing its

Continuous Monitoring Program (CMP). The CMP assesses and evaluates internal

controls, compliance with generally accepted accounting principles, and evidence

used to support that balances and activity reported in NASA’s financial

statements are accurate and complete by requiring Centers to perform a set of

control activities. Throughout FY 2009, the CMP has operated as designed. NASA

has identified exceptions through the execution of the control activities and

has generally tracked and resolved those exceptions in a timely manner.

Although much progress has been made in developing

policies, procedures, and controls to improve NASA’s financial processes and

systems, challenges remain. Specifically, during FY 2009, NASA management and

Ernst & Young LLP (E&Y) continued to identify deficiencies in the

Agency’s system of internal control, which impair NASA’s ability to timely

report accurate financial information. The most severe deficiency involves

NASA’s internal control over legacy property, plant, and equipment (PP&E).

As shown in the following table, this deficiency has been reported as a

material weakness for several years.

The

following is especially important. From page 11:

Standards of Ethical Conduct Compliance. There is a great

deal of interaction between NASA and the private sector, including both

industry and academia. Again, given that approximately 90 percent of NASA’s

budget is dedicated to contracts and grants, there is great incentive for

private sector interests to influence NASA employees. There is also substantial

interaction between NASA’s scientists and researchers and those working for

non-governmental entities, and incentives abound for such acts as sharing

information that is sensitive but unclassified. Many NASA employees often seek

to pursue financial opportunities in the private sector beyond their Government

employment. With the interchange of talented personnel between the public and

private sectors, the advent of term appointments, the use of Intergovernmental

Personnel Act appointments, and the use of contractors to meet personnel needs,

management is challenged to ensure that ethics laws and regulations applicable

to each category are identified and followed. It is imperative that NASA

employees, as stewards of NASA’s mission and budget, are aware of and comply

with the applicable ethics laws and regulations.

However,

Margolin filed a Freedom of Information Act Request on December 14, 2009. (See Ref5_f2_01.pdf and Ref5_f2_01a.pdf).

One of his requests was

11. Please send me documents relating to

a standard of ethics or conduct for NASA contractors.

NASA’s

tardy response to that item (Ref6_jm_nasa_foia2_response.pdf),

received February 16, 2010 was:

The link

to Federal Acquisition Regulations produces an interesting document (Ref7_08-12.pdf):

December 22, 2008

CONTRACTOR ETHICS

PURPOSE:

This Procurement Information Circular (PIC) is issued to call attention

to the new contractor ethics requirements and to advise acquisition personnel

of their roles and responsibilities in implementing the programs and processing

reports of violations under the program.

BACKGROUND:

Over the past year, two significant FAR rules related to contractor ethics have

been issued. In November of 2007, the FAR was revised to require

contractors to establish a written code of business ethics and conduct.

Furthermore, on December 12, 2008, the Contractor Business Ethics Compliance

Program and Disclosure Requirements went into effect, requiring contractors to

report criminal violations and overpayments.

Under the fist{sic} rule,

contractors are required to:

- Establish a

written code of business ethics (FAR 52.203-13)

- Establish an

internal control system that facilitates timely discovery of improper conduct

in connection with Government contracts and ensures that corrective action is

taken.

- Train their

employees in business ethics; promote business ethics awareness

The second rule builds upon the

first by additionally requiring contractors to:

- Timely

disclose any violations of Federal criminal law involving fraud, conflict

of interest, bribery, or gratuity violations found in Title 18 of the United

States Code; or a violation of the civil False Claims Act (31 U.S.C. 3729-3733)

to the Agency Office of the Inspector General, with a copy to the contracting

officer.

- Timely disclose

and remit any significant overpayments made by the Government.

Therefore:

1.

Contractors have to agree to disclose any violations of specified

Federal criminal laws that they commit.

2.

Contractors have to come up with their own written code of business

ethics.

If NASA requires (allows) Contractors to write their own

business ethics code, and there is no standard for judging the adequacy of the

Contractor’s ethics code, then NASA does not have a business ethics code for its

Contractors.

Reference 4 (NASA 2009

Management Challenges) refers to a Standards of Ethical Conduct Compliance for

NASA employees. However, NASA employees are working with Contractors who set

their own code of ethics.

5. As of February 2010 NASA has still failed to

get its financial house in order. NASA’s auditor refused to sign-off on its

latest audit.

Reference 8 - GAO United States Government

Accountability Office Testimony Before the Subcommittee on Space and

Aeronautics, Committee on Science and Technology, House of Representatives - NASA

Key Management and

Program Challenges, Statement of Cristina Chaplain, Director Acquisition

and Sourcing Management, February 3, 2010 - http://legislative.nasa.gov/hearings/2-3-10%20CHAPLAIN.pdf {Click here for Local Copy}

From page 7:

NASA has continually struggled to

put its financial house in order. GAO and others have reported for years on

these efforts.7 In fact, GAO

has made a number of recommendations to address NASA’s financial management

challenges. Moreover, the NASA Inspector General has identified financial

management as one of NASA’s most serious challenges. In a November 2008 report,

the Inspector General found continuing weaknesses in NASA’s financial

management process and systems, including internal controls over property

accounting. It noted that these deficiencies have resulted in disclaimed audits

of NASA’s financial statements since fiscal year 2003. The disclaimers were

largely attributed to data integrity issues and poor internal controls. NASA

has made progress in addressing some of these issues, but the recent disclaimer

on the fiscal year 2009 audit shows that more work needs to be done.

Here is footnote 7:

7 GAO, Property Management: NASA’s Goal of

Increasing Equipment Reutilization May Fall Short without Further Efforts, GAO-09-187

(Washington, D.C.: Jan. 30, 2009); GAO; Business Modernization: NASA Must

Consider Agencywide Needs to Reap the Full Benefits of Its Enterprise

Management System Modernization Effort, GAO-07-691 (Washington, D.C.: July 20,

2007); and GAO, Financial Management Systems: Additional Efforts Needed to

Address Key Causes of Modernization Failures, GAO-06-184 (Washington, D.C.:

Mar. 15, 2006).

6. NASA Administrator Bolden found it necessary

to issue a centerwide communication ordering all NASA personnel to cooperate with OIG

investigations and audits.

Reference 9 - This is

from SpaceRef: http://www.spaceref.com/news/viewsr.rss.html?pid=33246

Although the article gives a link to the NASA HQ web site

General Bolden’s announcement does not seem to be there.

Message from Administrator Charles

F. Bolden, Jr. - January 14, 2010 Transparency, Communication and Cooperation

STATUS REPORT

Date Released: Thursday, January

14, 2010

Source:

NASA HQ

Subject:

Message from Administrator Charles F. Bolden,

Jr. - January 14, 2010 Transparency, Communication and Cooperation

From:

Centerwide Announcement

Date:

Thursday, January 14, 2010

Message from Administrator Charles

F. Bolden, Jr. - January 14, 2010 Transparency, Communication and Cooperation

President Obama has made it clear

that he is committed to a more transparent and responsive Federal Government. I

believe that NASA should be a leader in implementing that goal. Accordingly,

whether we are referring to the Agency’s treatment of requests under the

Freedom of Information Act, answering questions from Congress or cooperating

with our Inspector General in Agency audits or investigations, I expect that we

will respond both promptly and thoroughly.

As I know you realize and I hope

you appreciate, the NASA Office of Inspector General (OIG) performs a valuable

function at the Agency with both its audits and its investigations. I fully

support the OIG’s efforts to eradicate fraud, waste and abuse, as well as its

role in making the Agency more efficient and more effective. While cooperation

with OIG audits and investigations is mandated by Federal laws and regulations,

NASA employees should readily and fully cooperate whenever an OIG

representative seeks access to personnel, facilities, records, reports,

databases, or documents because it is the right thing to do. Leadership should

also ensure that no unduly burdensome requirements are imposed on OIG auditors

or investigators carrying out their important duties. We also need to

understand that while OIG personnel generally will state the reason for their

requests, they are under no obligation to do so and sometimes cannot do so.

The OIG also serves as the point of

contact for NASA employees to report possible criminal activity, fraud, waste,

abuse and mismanagement involving Agency funds or employees.

As we begin this new decade, let’s

renew our commitment to strengthening NASA’s traditional values of openness,

honesty and transparency.

With best regards for the New Year,

Charles F. Bolden, Jr.

Let’s see if General Bolden and Deputy Administrator Garver can get

NASA’s house in order.

Jed Margolin

Virginia City Highlands, NV

March 7, 2010